Firms that invest in hedge funds on behalf of large institutions and wealthy individuals—an industry that got its U.S. start in Chicago more than 40 years ago—are recasting their businesses as clients unhappy with an extra layer of fees are bypassing the middlemen.

In the most striking local example, Chicago-based Grosvenor Capital Management LP, a pioneer in creating funds of hedge funds, paid $200 million this month to buy a private-equity business. It’s also starting a mutual fund, as are smaller rivals in the city. And all the firms are offering to tailor hedge-fund investments to individual client needs, as opposed to one-size-fits-all funds.

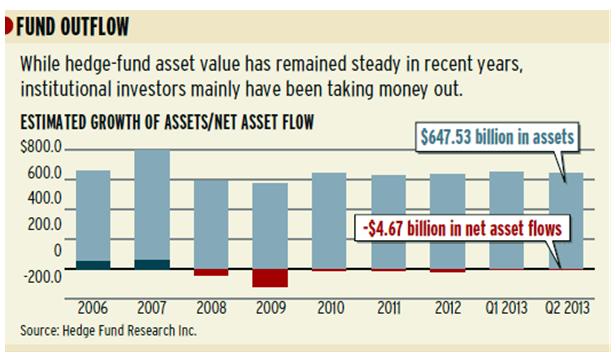

The moves follow five consecutive years in which pension funds, endowments and foundations pulled money out of funds of hedge funds. While funds of funds still manage $647 billion in assets, that’s down from $800 billion in 2007, according to Hedge Fund Research Inc. Now the firms are wading into new asset management territory and taking on new competition.

“As the industry looks forward, we’re all thinking about how do we continue to be relevant in the 21st century as fees are coming under greater scrutiny,” says Scott Schweighauser, president of Chicago-based fund of hedge funds manager Aurora Investment Management LLC. “Given moderate return expectations, fees are a more critical part of overall returns.”

The fund of hedge funds industry came to life in the U.S. in 1971 when Chicago investment professional Dick Elden founded Grosvenor. The model gained ground over the next three decades as institutional investors turned to such managers for help in navigating complex and opaque hedge-fund investment strategies. According to Towers Watson & Co., Grosvenor grew to become the fifth-largest player in the industry, behind others such as No. 1 Blackstone Group LP, based in New York.

After hedge-fund managers’ performance foundered during the financial crisis and manager Bernie Madoff lost billions of customer funds, investors began to question paying fund of hedge fund managers an additional fee if they couldn’t count on them to provide better returns and more security.

“There were some pretenders in the fund of hedge funds industry in the fat years,” says Brian Ziv, who leads a fund of hedge funds unit at William Blair & Co. in Chicago. “When the tide went out, some of them got caught wearing Madoff.”

Institutional investors have begun burnishing their own hedge-fund investing acumen in recent years, allowing them to bypass fund of fund managers and invest directly with hedge funds. The Illinois Teachers’ Retirement System, the largest pension fund in the state, has announced it will eliminate one of its two fund of hedge fund managers later this year, choosing between Grosvenor and rival K2 Advisors LLC of Stamford, Conn.

“Many of our clients are prepared to invest directly, whereas a few years ago they might have thought that was too bold,” says Peter Hill, a partner at Hewitt EnnisKnupp in Chicago and consultant to institutional investors.

NEW SERVICES

The shift has prompted the fund of hedge fund firms to woo new retail customers and offer new services to existing clients, such as private-equity options or increased hedge-fund counsel.

There were some pretenders in the fund of hedge funds industry in the fat years.”

Aurora decided this year to begin offering its first mutual fund, looking to tap the retail market for hedge-fund investments. Similar to its role as a fund of hedge funds manager, Aurora acts as investment manager for the mutual fund, selecting hedge-fund managers who invest a portion of the fund’s assets in a particular strategy.

Other fund of hedge fund managers in Chicago, including Mesirow Advanced Strategies President Tom Macina, have opted not to start mutual funds, questioning whether they can provide the easy exit retail investors want.

At Grosvenor, where hedge-fund assets under management have slipped slightly in recent years to $23 billion, its custom account “solutions business” has risen to $15 billion of that total, CEO Michael Sacks says. And now, it has an $18 billion private-equity business as well.

“The benefits of scale and customization have made the value proposition of the solutions business better than it has ever been,” Mr. Sacks says.

Source: http://www.chicagobusiness.com