Debt Investing Concept: Credit Curves

While this post is more particular to high yield and investment grade bonds, than to distressed investing, I believe it is an important concept considering what is going on in certain pockets of the market today. A credit curve is essentially the spread over treasuries of various maturities for a single bond issuer. The greater the difference between the front end (near term maturities) versus the long end (longer maturities) determines the steepness of the credit curve.

Generally speaking, more cyclical industries will have a steeper credit curve. Retail for instance will generally have a pretty steep credit curve. This reflects the fact that the probability of default increases cumulatively over time. This can also be seen on CDS curves. For example, see below for the CDS term structure for Home Depot (HD) as of today and last year at this time.

The top line above represents the curve as of last year. And the upward sloping one represents as of today. What is this telling us?

When a curve is flat, it is essentially saying that the probability of default is fairly uniform through the tenure of the projection periods. When it is upward sloping it signifies that the probability of default in the near term is far less likely than the outer years.

Look at the chart below:

This is the BP curve. Again the yellowish line represents last year, with the red line representing the current term structure. The curve is inverted which means that investors believe that there is a higher likelihood that BP default in the near term relative to the outer years.

If you have access to a Bloomberg, you can run the function CDSW on any single name CDS to determine the implied default probability of the underlying credit. For example, in BP’s case, the 1 year CDS is trading at (who knows where it opens) 550, which implies a 1 year default probability of near 10%.

If an investor has an opinion on the relative likelihoods of default probabilities / credit spread widening across a credit curve, he or she can reflect it in a curve steepener trade or a flattener trade. If I thought all this press commentary about BP filing was just speculation, I could sell the near term CDS and buy the longer dated CDS. If BP files for bankruptcy tomorrow, I would be net hedged (both swaps trigger, I would receive a dollar amount from my buying of protection and then deliver it as I sell protection). If BP makes it a few years, my 1 year CDS sale expires worthless and I collect the premium.

The problem with this though arises as you are duration mismatched. Similar to bonds, the further you go out in maturity, the more sensitivity a particular CDS contract has to spread changes. A general rule of thumb is divide the number of years to maturity of a CDS contract by 100 and that is how many basis points of spread represents 1 point of price movement (important for mark to market). So if I buy 5 year HD protection, each 20 bps of movement will change the contract market value by 1 point (100/5 years = 20 bps).

Many people in the fixed income world live and down by these trades. They are taking very little risk by entering into many offsetting contracts, collecting premiums off the basis, and doing it in size.

By looking at the credit curve and CDS term structure, an investor can find relative value in the fixed income space. For example, if I look out into the market and see that Home Depot’s 5-30 is 100 bps steep whereas Lowe’s is 50 bps steep, there could be a relative value opportunity there. This is even more magnified by given how steep the treasury curve is.

Now distressed is a little bit different. As distressed investors we can play a certain situation very differently considering how we view the credit.

If I feel a credit can make it next year, but not the following few years, I may buy the nearest term bond and hedge myself with buying slightly longer duration CDS or purchasing puts on the equity.

If I think all will by rosy, I may play either the near term or the long end depending on how steep the credit curve is.

If I feel a credit is doomed to failure, I would buy the LOWEST priced bond. Because bonds similar in nature (i.e. pari passu) are treated equally in a reorganization, I want to try to “create” the investment at the lowest cost possible to capture the most upside. If I think I am getting 80 in a re-org, and I have the choice between identical bonds, one maturing in 5 years and one maturing in 30 years, at 60 and 40 respectively, I would always by the 40 dollar bond because I will make 100% on my investment versus 33%.

As companies get closer and closer to distressed, their bonds will begin to trade on an a level where their recoveries are identical. Discrepancies arise based on accrued interest. If a company has a bond with a 5% coupon and another with a 10% coupon, the latter will be entitled to more accrued interest and thus his claim will be higher and market prices will reflect this.

The point of all this is that there is a wealth of information in credit curves for investors ranging from IG to distressed. One needs to understand why a curve is shaped a particular way and how it got there. Most importantly though, an investor needs to understand what the credit curve is saying about risks reflected in the market price of the underlying securities and whether the market is overestimating, or underestimating, the credit / default risk of this company. You can look up the odds using “CDSW” – and with those odds you can place wagers when you truly disagree with the market.

Source : distressed-debt-investing.com

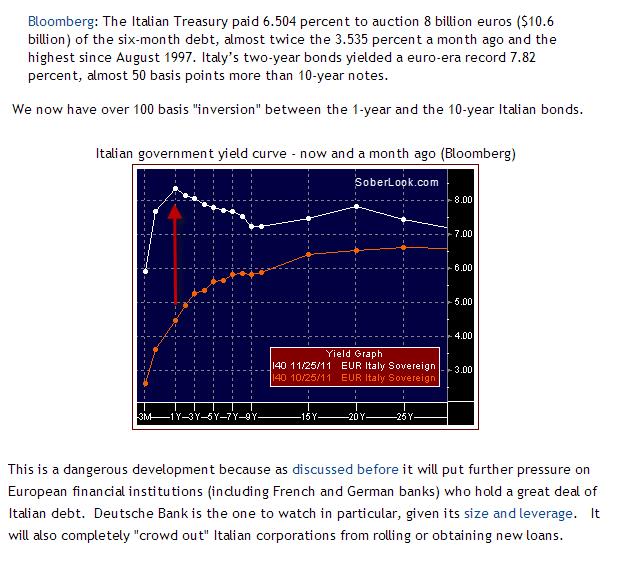

Example :